Extended example : emhawkes package

Kyungsub Lee

2025-08-26

Source:vignettes/extended_example.Rmd

extended_example.RmdBasic Hawkes model

Univariate Hawkes process

This subsection outlines the steps for constructing, running

simulations, and estimating a univariate Hawkes model. To begin, create

an hspec object, which defines the Hawkes model. The S4

class hspec contains slots for the model parameters:

mu, alpha, beta,

dimens, rmark, and impact.

In a univariate model, the basic parameters of the

model—mu, alpha, and beta—can be

given as numeric values. If numeric values are provided, they will be

converted to matrices. Below is an example of a univariate Hawkes model

without a mark.

mu1 <- 0.3; alpha1 <- 1.2; beta1 <- 1.5

hspec1 <- new("hspec", mu = mu1, alpha = alpha1, beta = beta1)

show(hspec1)

#> An object of class "hspec" of 1-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.3

#>

#> Slot alpha:

#> [,1]

#> [1,] 1.2

#>

#> Slot beta:

#> [,1]

#> [1,] 1.5The function hsim implements simulation where the input

arguments are hspec, size, and the initial

values of the intensity component process,

lambda_component0, and the initial values of the Hawkes

processes, N0. More precisely, the intensity process of the

basic univariate Hawkes model is represented by

where the lambda_component0 denotes

If lambda_component0 is not provided, the internally

determined initial values for the intensity process are used. If

size is sufficiently large, the exact value of

lambda_component0 may not be important. The default initial

value of the counting process, N0, is zero.

set.seed(1107)

res1 <- hsim(hspec1, size = 1000)

summary(res1)

#> -------------------------------------------------------

#> Simulation result of exponential (marked) Hawkes model.

#> Realized path :

#> arrival N1 mark lambda1

#> [1,] 0.00000 0 0 0.90000

#> [2,] 0.97794 1 1 0.43838

#> [3,] 1.09001 2 1 1.43128

#> [4,] 1.28999 3 1 2.02711

#> [5,] 1.53225 4 1 2.33527

#> [6,] 1.65001 5 1 3.01139

#> [7,] 2.51807 6 1 1.36377

#> [8,] 2.81710 7 1 1.74553

#> [9,] 2.87547 8 1 2.72378

#> [10,] 3.16415 9 1 2.65016

#> [11,] 3.51378 10 1 2.40131

#> [12,] 4.22355 11 1 1.43843

#> [13,] 16.96752 12 1 0.30000

#> [14,] 17.71654 13 1 0.69015

#> [15,] 19.10293 14 1 0.49874

#> [16,] 24.06354 15 1 0.30082

#> [17,] 24.09256 16 1 1.44967

#> [18,] 28.40173 17 1 0.30366

#> [19,] 28.53743 18 1 1.28198

#> [20,] 28.56702 19 1 2.38725

#> ... with 980 more rows

#> -------------------------------------------------------The results of hsim is an S3 class hreal,

which consists of hspec, inter_arrival,

arrival, type, mark,

N, Nc, lambda,

lambda_component, rambda,

rambda_component.

hspecis the model specification.inter_arrivalis the inter-arrival time of every event.arrivalis the cumulative sum ofinter_arrival.typeis the type of events, i.e., for , and is used for a multivariate model.markis a numeric vector that represents additional information for the event.lambdarepresents , which is the left continuous and right limit version.The right continuous version of intensity is

rambda.lambda_componentrepresents , andrambda_componentis the right continuous version.

inter_arrival, type, mark,

N, and Nc start at zero. Using the

summary() function, one can print the first 20 elements of

arrival, N, and lambda. The

print() function can also be used.

By definition, we have

lambda == mu + lambda_component.

# first and third columns are the same

cbind(res1$lambda[1:5], res1$lambda_component[1:5], mu1 + res1$lambda_component[1:5])

#> [,1] [,2] [,3]

#> [1,] 0.900000 0.600000 0.900000

#> [2,] 0.438383 0.138383 0.438383

#> [3,] 1.431282 1.131282 1.431282

#> [4,] 2.027111 1.727111 2.027111

#> [5,] 2.335269 2.035269 2.335269For all rows except the first, rambda equals

lambda + alpha in this model.

# second and third columns are the same

cbind(res1$lambda[1:5], res1$rambda[1:5], res1$lambda[1:5] + alpha1)

#> [,1] [,2] [,3]

#> [1,] 0.900000 0.900000 2.100000

#> [2,] 0.438383 1.638383 1.638383

#> [3,] 1.431282 2.631282 2.631282

#> [4,] 2.027111 3.227111 3.227111

#> [5,] 2.335269 3.535269 3.535269Additionally, verify that the exponential decay is accurately represented in the model.

# By definition, the following two are equal:

res1$lambda[2:6]

#> [1] 0.438383 1.431282 2.027111 2.335269 3.011391

mu1 + (res1$rambda[1:5] - mu1) * exp(-beta1 * res1$inter_arrival[2:6])

#> [1] 0.438383 1.431282 2.027111 2.335269 3.011391The log-likelihood function is calculated using the

logLik method. In this context, the inter-arrival times and

hspec are provided as inputs to the function.

logLik(hspec1, inter_arrival = res1$inter_arrival)

#> The initial values for intensity processes are not provided. Internally determined initial values are used.

#> loglikelihood

#> -214.2385The likelihood estimation is performed using the hfit

function. The specification of the initial parameter values,

hspec0, is required. Note that only

inter_arrival is needed for this univariate model. For more

accurate simulation, it is recommended to specify lambda0,

the initial value of the lambda component. If lambda0 is

not provided, the function uses internally determined initial values. By

default, the BFGS method is employed for numerical optimization.

# initial value for numerical optimization

mu0 <- 0.5; alpha0 <- 1.0; beta0 <- 1.8

hspec0 <- new("hspec", mu = mu0, alpha = alpha0, beta = beta0)

# the intial values are provided through hspec

mle <- hfit(hspec0, inter_arrival = res1$inter_arrival)

summary(mle)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 24 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -213.4658

#> 3 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.33641 0.03475 9.682 <2e-16 ***

#> alpha1 1.16654 0.09608 12.141 <2e-16 ***

#> beta1 1.52270 0.12468 12.213 <2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------Bivariate Hawkes model

The intensity process of a basic bivariate Hawkes model is defined by

In a bivariate model, the parameters within the slots of

hspec are matrices. Specifically, mu is a

2-by-1 matrix, while alpha and beta are 2-by-2

matrices.

rmark is a random number generating function for marks

and is not used in non-mark models. lambda_component0 is a

2-by-2 matrix that represents the initial values of

lambda_component, which includes the set of values

lambda11, lambda12, lambda21, and

lambda22. The intensity processes are represented by

The terms

are referred to as lambda components, and lambda0

represents $_{ij}(0). The parameterlambda_component0` can

be omitted in this model, in which case internally determined initial

values will be used.

mu2 <- matrix(c(0.2), nrow = 2)

alpha2 <- matrix(c(0.5, 0.9, 0.9, 0.5), nrow = 2, byrow = TRUE)

beta2 <- matrix(c(2.25, 2.25, 2.25, 2.25), nrow = 2, byrow = TRUE)

hspec2 <- new("hspec", mu=mu2, alpha=alpha2, beta=beta2)

print(hspec2)

#> An object of class "hspec" of 2-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.2

#> [2,] 0.2

#>

#> Slot alpha:

#> [,1] [,2]

#> [1,] 0.5 0.9

#> [2,] 0.9 0.5

#>

#> Slot beta:

#> [,1] [,2]

#> [1,] 2.25 2.25

#> [2,] 2.25 2.25To perform a simulation, use the hsim function.

set.seed(1107)

res2 <- hsim(hspec2, size=1000)

summary(res2)

#> -------------------------------------------------------

#> Simulation result of exponential (marked) Hawkes model.

#> Realized path :

#> arrival N1 N2 mark lambda1 lambda2

#> [1,] 0.00000 0 0 0 0.52941 0.52941

#> [2,] 0.57028 1 0 1 0.29130 0.29130

#> [3,] 1.66175 1 1 1 0.25073 0.28505

#> [4,] 2.17979 1 2 1 0.49638 0.38238

#> [5,] 2.47685 1 3 1 0.81319 0.54975

#> [6,] 2.64001 2 3 1 1.24825 0.78866

#> [7,] 2.70249 3 3 1 1.54519 1.49341

#> [8,] 2.94547 4 3 1 1.26810 1.46968

#> [9,] 3.39313 4 4 1 0.77271 0.99242

#> [10,] 3.52533 4 5 1 1.29379 1.15989

#> [11,] 3.56971 5 5 1 2.00432 1.52115

#> [12,] 3.70761 5 6 1 1.88965 1.82866

#> [13,] 4.30122 5 7 1 0.88106 0.75983

#> [14,] 4.34337 6 7 1 1.63800 1.16393

#> [15,] 4.40222 7 7 1 1.89764 1.83275

#> [16,] 4.58943 8 7 1 1.64219 1.86211

#> [17,] 5.14665 9 7 1 0.75437 0.93131

#> [18,] 5.18186 9 8 1 1.17407 1.70707

#> [19,] 5.36167 9 9 1 1.45050 1.53925

#> [20,] 5.89118 10 9 1 0.85331 0.75875

#> ... with 980 more rows

#> -------------------------------------------------------In multivariate models, type is crucial as it represents

the type of event.

# Under bi-variate model, there are two types, 1 or 2.

res2$type[1:10]

#> [1] 0 1 2 2 2 1 1 1 2 2In multivariate models, the column names of N are

N1, N2, N3, and so on.

res2$N[1:3, ]

#> N1 N2

#> [1,] 0 0

#> [2,] 1 0

#> [3,] 1 1Similarly, the column names of lambda are

lambda1, lambda2, lambda3, and so

on.

res2$lambda[1:3, ]

#> lambda1 lambda2

#> [1,] 0.5294118 0.5294118

#> [2,] 0.2913028 0.2913028

#> [3,] 0.2507301 0.2850475The column names of lambda_component are

lambda_component11, lambda_component12,

lambda_component13, and so on.

res2$lambda_component[1:3, ]

#> lambda11 lambda12 lambda21 lambda22

#> [1,] 0.11764706 0.211764706 0.21176471 0.117647059

#> [2,] 0.03260813 0.058694641 0.05869464 0.032608134

#> [3,] 0.04569443 0.005035631 0.08224997 0.002797573By definition, the following two expressions are equivalent:

mu2[1] + rowSums(res2$lambda_component[1:5, c("lambda11", "lambda12")])

#> [1] 0.5294118 0.2913028 0.2507301 0.4963769 0.8131889

res2$lambda[1:5, "lambda1"]

#> [1] 0.5294118 0.2913028 0.2507301 0.4963769 0.8131889From the results, we obtain vectors of realized

inter_arrival and type. A bivariate model

requires both inter_arrival and type for

estimation.

inter_arrival2 <- res2$inter_arrival

type2 <- res2$typeThe log-likelihood is computed using the logLik

function.

logLik(hspec2, inter_arrival = inter_arrival2, type = type2)

#> The initial values for intensity processes are not provided. Internally determined initial values are used.

#> loglikelihood

#> -974.2809Maximum log-likelihood estimation is performed using the

hfit function. In this process, the parameter values in

hspec0, such as mu, alpha, and

beta, serve as starting points for the numerical

optimization. For illustration purposes, we set

hspec0 <- hspec2. Since the true parameter values are

unknown in practical applications, these initial guesses are used. The

realized inter_arrival and type data are

utilized for estimation.

hspec0 <- hspec2

mle <- hfit(hspec0, inter_arrival = inter_arrival2, type = type2)

summary(mle)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 36 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -970.1408

#> 4 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.19095 0.01636 11.671 < 2e-16 ***

#> alpha1.1 0.48217 0.07405 6.511 7.45e-11 ***

#> alpha1.2 0.98625 0.09495 10.387 < 2e-16 ***

#> beta1.1 2.07987 0.16952 12.269 < 2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------

coef(mle)

#> mu1 alpha1.1 alpha1.2 beta1.1

#> 0.1909541 0.4821725 0.9862542 2.0798691

miscTools::stdEr(mle)

#> mu1 alpha1.1 alpha1.2 beta1.1

#> 0.01636127 0.07405118 0.09495461 0.16952428Parameter setting

This subsection explores the relationship between parameter settings

and the estimation procedure in a multivariate Hawkes model. The number

of parameters to be estimated in the model is influenced by how we

configure parameter slots such as mu, alpha,

and beta in hspec0, which specifies the

initial values.

Since the parameter slot alpha is a matrix, its elements

can either be the same or different. Consequently, the number of

parameters estimated varies depending on whether the initial settings

have identical or distinct elements.

For example, if alpha[1,1] and alpha[1,2]

in hspec0 are initially set to different values, the

numerical procedure will estimate alpha[1,1] and

alpha[1,2] separately. Conversely, if

alpha[1,1] and alpha[1,2] are the same in the

initial setting, the estimation procedure treats these parameters as

identical in the model, thus estimating only one value.

Recall that the example in the previous section features a symmetric

Hawkes model, where the matrix alpha is symmetric and all

elements of beta are identical.

print(hspec2)

#> An object of class "hspec" of 2-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.2

#> [2,] 0.2

#>

#> Slot alpha:

#> [,1] [,2]

#> [1,] 0.5 0.9

#> [2,] 0.9 0.5

#>

#> Slot beta:

#> [,1] [,2]

#> [1,] 2.25 2.25

#> [2,] 2.25 2.25In the first estimation example, the initial value of

alpha0 is a matrix where all elements are set to the same

value of 0.75. In this configuration, hfit assumes that

alpha11, alpha12, alpha21, and

alpha22 are identical in the model, even if the actual

parameters have different values. Similarly, the parameter matrices

mu0 and beta0 are treated in the same

manner.

mu0 <- matrix(c(0.15, 0.15), nrow = 2)

alpha0 <- matrix(c(0.75, 0.75, 0.75, 0.75), nrow = 2, byrow=TRUE)

beta0 <- matrix(c(2.6, 2.6, 2.6, 2.6), nrow = 2, byrow=TRUE)

hspec0 <- new("hspec", mu=mu0, alpha=alpha0, beta=beta0)

summary(hfit(hspec0, inter_arrival = res2$inter_arrival, type = res2$type))

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 44 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -979.5687

#> 3 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.19125 0.01636 11.69 <2e-16 ***

#> alpha1.1 0.73981 0.05951 12.43 <2e-16 ***

#> beta1.1 2.09707 0.16524 12.69 <2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------Note that in the above result, alpha1.1 falls somewhere

between the original values of alpha1.1 = 0.5 and

alpha1.2 = 0.9.

In the following second example, the elements of alpha0

are not identical but are symmetric, reflecting the original values used

in the simulation. Specifically, we have alpha11 == alpha22

and alpha12 == alpha21 in alpha0, so

alpha11 and alpha12 will be estimated

differently.

mu0 <- matrix(c(0.15, 0.15), nrow = 2)

alpha0 <- matrix(c(0.75, 0.751, 0.751, 0.75), nrow = 2, byrow=TRUE)

beta0 <- matrix(c(2.6, 2.6, 2.6, 2.6), nrow = 2, byrow=TRUE)

hspec0 <- new("hspec", mu=mu0, alpha=alpha0, beta=beta0)

summary(hfit(hspec0, inter_arrival = res2$inter_arrival, type = res2$type))

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 30 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -970.1408

#> 4 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.19095 0.01643 11.619 < 2e-16 ***

#> alpha1.1 0.48226 0.07421 6.499 8.1e-11 ***

#> alpha1.2 0.98626 0.09538 10.341 < 2e-16 ***

#> beta1.1 2.08008 0.17303 12.021 < 2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------In the third example, the estimation is performed under the

assumption that mu1 and mu2 may differ, even

though they are the same in the original model.

mu0 <- matrix(c(0.15, 0.14), nrow = 2)

alpha0 <- matrix(c(0.75, 0.751, 0.751, 0.75), nrow = 2, byrow=TRUE)

beta0 <- matrix(c(2.6, 2.6, 2.6, 2.6), nrow = 2, byrow=TRUE)

hspec0 <- new("hspec", mu=mu0, alpha=alpha0, beta=beta0)

summary(hfit(hspec0, inter_arrival = res2$inter_arrival, type = res2$type))

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 42 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -969.9914

#> 5 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.18300 0.02154 8.495 < 2e-16 ***

#> mu2 0.19872 0.02203 9.020 < 2e-16 ***

#> alpha1.1 0.48149 0.07425 6.484 8.91e-11 ***

#> alpha1.2 0.98720 0.09556 10.331 < 2e-16 ***

#> beta1.1 2.07973 0.17094 12.166 < 2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------By setting reduced = FALSE, all parameters are

estimated.

summary(hfit(hspec2, inter_arrival = res2$inter_arrival, type = res2$type, reduced=FALSE))

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 51 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -966.5055

#> 10 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.17997 0.02312 7.784 7.05e-15 ***

#> mu2 0.20060 0.02442 8.214 < 2e-16 ***

#> alpha1.1 0.44726 0.16627 2.690 0.00714 **

#> alpha2.1 1.17743 0.22909 5.140 2.75e-07 ***

#> alpha1.2 0.97048 0.14242 6.814 9.47e-12 ***

#> alpha2.2 0.48979 0.15398 3.181 0.00147 **

#> beta1.1 2.52210 1.16375 2.167 0.03022 *

#> beta2.1 3.15498 0.67702 4.660 3.16e-06 ***

#> beta1.2 1.80167 0.25695 7.012 2.35e-12 ***

#> beta2.2 1.51338 0.54476 2.778 0.00547 **

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------The same logic applies to all higher-dimensional models.

Residual process

The residual process can be extracted using the logLik()

function by setting infer = TRUE. When this option is

enabled, the logLik function returns a list that includes

the log-likelihood, inferred intensities, and the residual process. Note

that the inference is based on the object passed to the

logLik function. In the returned object,

res_process1 represents the residual process.

hrp <- new("hspec", mu = 0.3, alpha = 1.2, beta = 1.5)

res_rp <- hsim(hrp, size = 1000)

# inferred result

infered_res <- logLik(hrp, res_rp$inter_arrival, infer = TRUE)

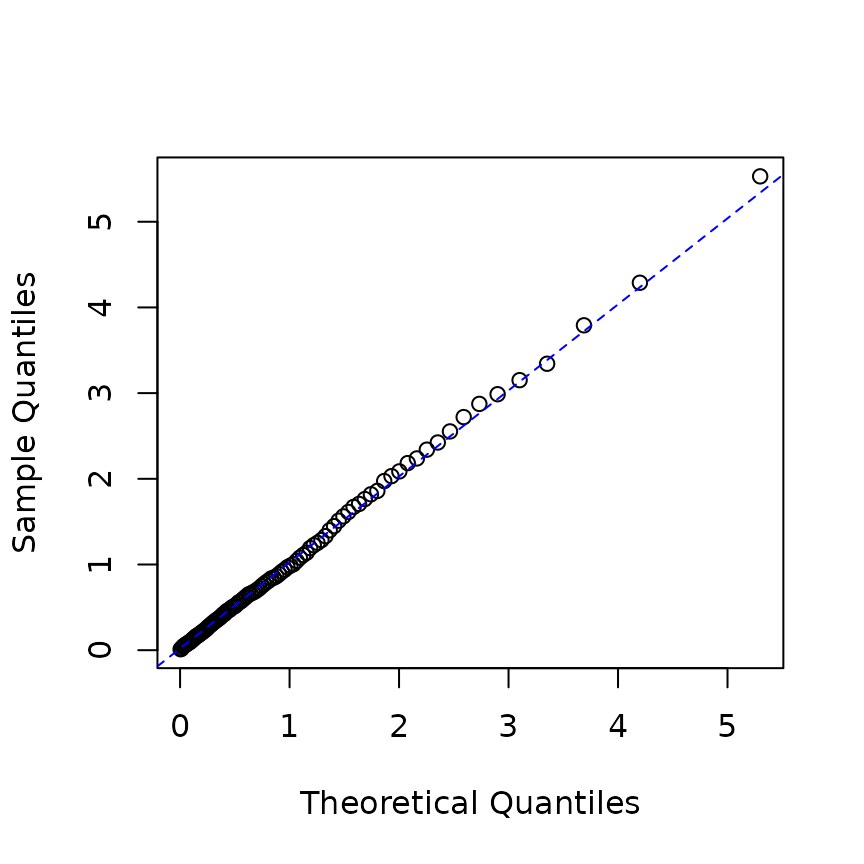

## QQ-plot

p <- ppoints(100)

q <- quantile(infered_res$res_process1, p = p)

plot(qexp(p), q, xlab="Theoretical Quantiles",ylab="Sample Quantiles")

qqline(q, distribution=qexp,col="blue", lty=2)

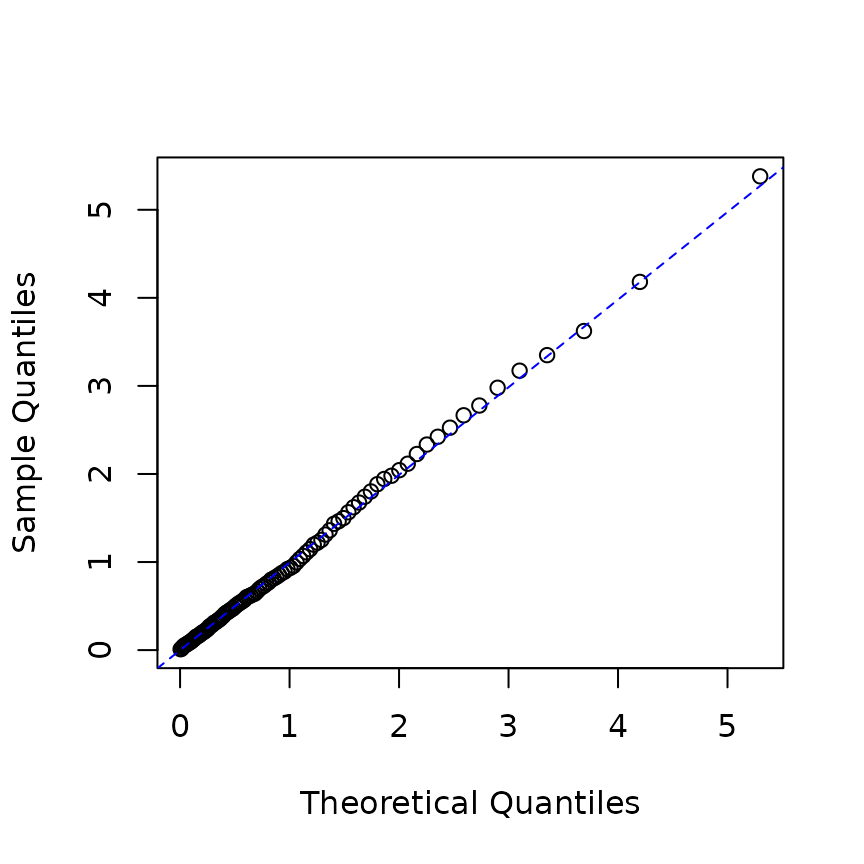

In practical scenarios, the parameter values are usually unknown, so the model may be estimated before computing the residual processes.

# estimation

mle_rp <- hfit(new("hspec", mu = 0.2, alpha = 1, beta = 2),

res_rp$inter_arrival)

# construct hspec from estimation result

he <- new("hspec", mu = coef(mle_rp)["mu1"],

alpha = coef(mle_rp)["alpha1"], beta = coef(mle_rp)["beta1"])

# infer intensity

infered_res <- logLik(he, res_rp$inter_arrival, res_rp$type, infer = TRUE)

rpe <- infered_res$res_process1

p <- ppoints(100)

q <- quantile(rpe, p=p)

plot(qexp(p), q, xlab="Theoretical Quantiles",ylab="Sample Quantiles")

qqline(q, distribution=qexp,col="blue", lty=2)

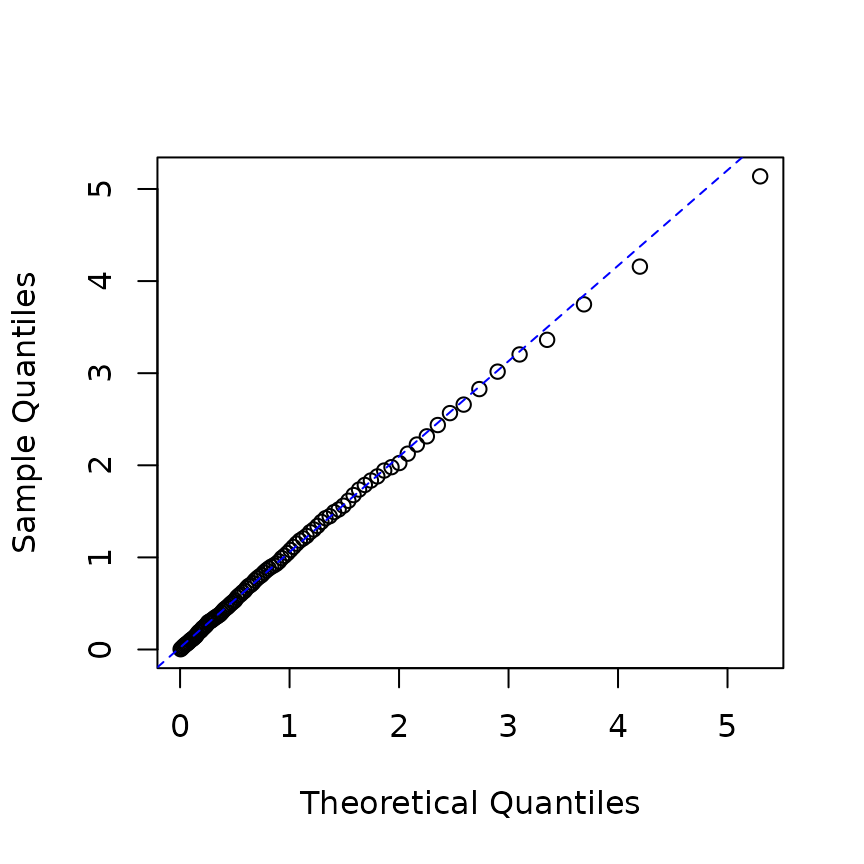

In an

-dimensional

model, we can compute the residuals in a similar manner. In this case,

the object returned by the logLik function contains

residual processes. For example, in the following code,

infer_res2$res_process1 and

infer_res2$res_process2 represent the residual processes

for each type.

hrp2 <- new("hspec", mu = rep(0.3, 2),

alpha = matrix(c(1.2, 1.5, 1.5, 1.2), nrow=2),

beta = matrix(rep(3, 4), nrow=2))

res_hrp2 <- hsim(hrp2, size = 2000)

infer_res2 <- logLik(hrp2, res_hrp2$inter_arrival, res_hrp2$type, infer = TRUE)

p <- ppoints(100)

q <- quantile(c(infer_res2$res_process1, infer_res2$res_process2), p=p)

plot(qexp(p), q, xlab="Theoretical Quantiles",ylab="Sample Quantiles")

qqline(q, distribution=qexp,col="blue", lty=2)

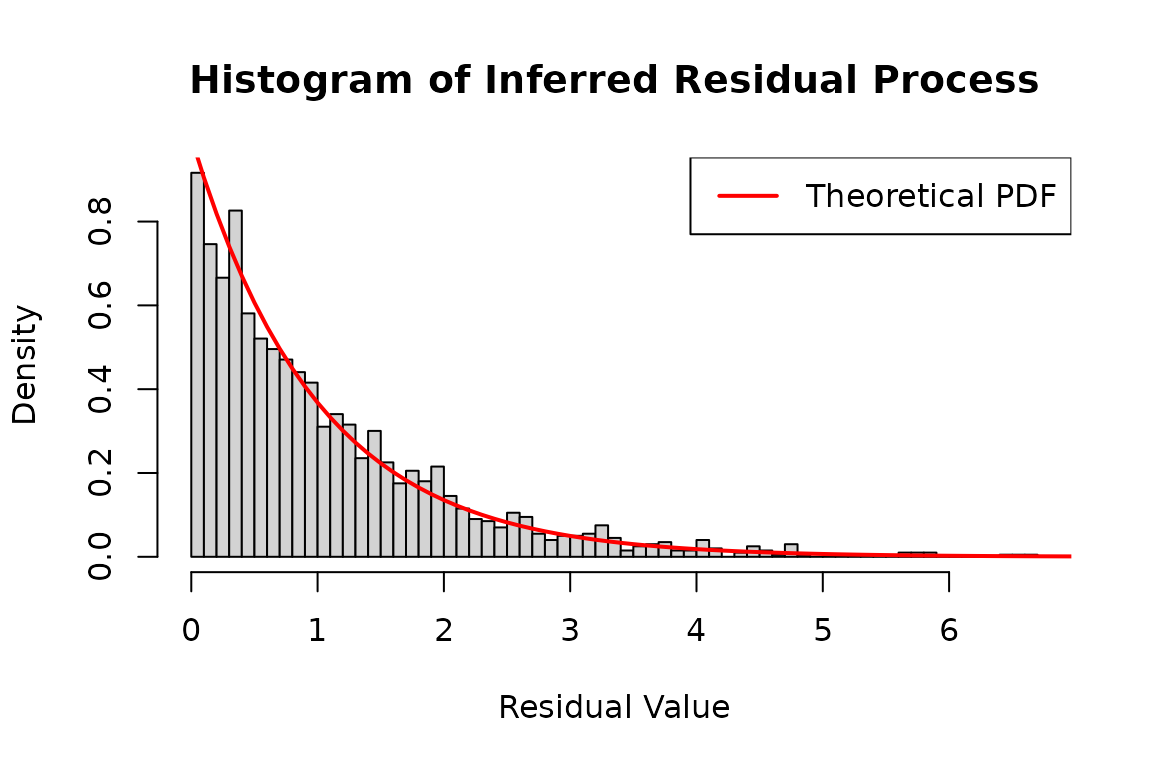

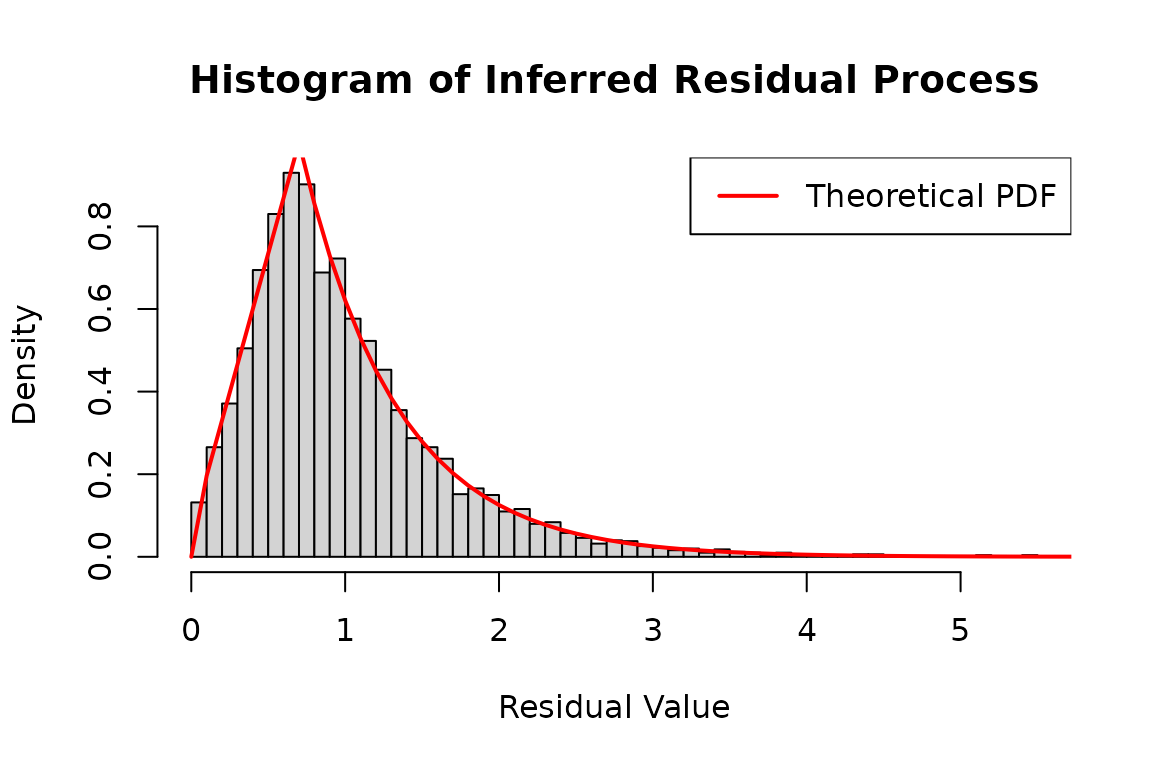

# Infer the residual process using the log-likelihood method

# 'infer_res_dh1' contains the inferred process data based on the inter-arrival times

hist(

c(infer_res2$res_process1, infer_res2$res_process2),

breaks = 50,

probability = TRUE,

main = "Histogram of Inferred Residual Process",

xlab = "Residual Value",

ylab = "Density"

)

x <- seq(0, 8, 0.1)

lines(

x,

dexp(x),

col = 'red',

lwd = 2

)

legend("topright", legend = "Theoretical PDF", col = "red", lwd = 2)

More complicated model

Multi-kernel model

In a multi-kernel Hawkes model, type_col_map is required

for hspec. type_col_map is a list that

represents the mapping between type and column number. For example,

consider a bi-variate multi-kernel model:

where

with matrix and denoting kernel number.

For example, in a bi-variate Hawkes model with two kernels, the intensity processes are

The parameter matrix is defined by

and we should specify which columns of matrix are associated with which .

mu <- matrix(c(0.02, 0.02), nrow=2)

beta_1 <- matrix(rep(10, 4), nrow=2)

beta_2 <- matrix(rep(1, 4), nrow=2)

beta <- cbind(beta_1, beta_2)

alpha_1 <- matrix(c(3, 2,

2, 3), nrow=2, byrow=TRUE)

alpha_2 <- matrix(c(0.3, 0.2,

0.2, 0.3), nrow=2, byrow=TRUE)

alpha <- cbind(alpha_1, alpha_2)

print(alpha)

#> [,1] [,2] [,3] [,4]

#> [1,] 3 2 0.3 0.2

#> [2,] 2 3 0.2 0.3Note that

is multiplied by first and third columns of

and

is multiplied by second and fourth columns of

and hence type_col_map is

type_col_map <- list(c(1,3), # columns for dN1

c(2,4)) # columns for dN2

type_col_map

#> [[1]]

#> [1] 1 3

#>

#> [[2]]

#> [1] 2 4where type i is associated with columns of

type_col_map[[i]]. Thus,

cat("Part of alpha associated with N1: \n")

#> Part of alpha associated with N1:

alpha[, type_col_map[[1]]] # associated with N1

#> [,1] [,2]

#> [1,] 3 0.3

#> [2,] 2 0.2

cat("Part of alpha associated with N2: \n")

#> Part of alpha associated with N2:

alpha[, type_col_map[[2]]] # associated with N2

#> [,1] [,2]

#> [1,] 2 0.2

#> [2,] 3 0.3

cat("Part of beta associated with N1: \n")

#> Part of beta associated with N1:

beta[, type_col_map[[1]]] # associated with N1

#> [,1] [,2]

#> [1,] 10 1

#> [2,] 10 1

cat("Part of beta associated with N2: \n")

#> Part of beta associated with N2:

beta[, type_col_map[[2]]] # associated with N2

#> [,1] [,2]

#> [1,] 10 1

#> [2,] 10 1

h <- new("hspec", mu = mu, alpha = alpha, beta=beta, type_col_map = type_col_map)

h

#> An object of class "hspec" of 2-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.02

#> [2,] 0.02

#>

#> Slot alpha:

#> [,1] [,2] [,3] [,4]

#> [1,] 3 2 0.3 0.2

#> [2,] 2 3 0.2 0.3

#>

#> Slot beta:

#> [,1] [,2] [,3] [,4]

#> [1,] 10 10 1 1

#> [2,] 10 10 1 1

#>

#> Slot type_col_map:

#> [[1]]

#> [1] 1 3

#>

#> [[2]]

#> [1] 2 4In addition, lambda_component0 should be provided for

simulation and estimation.

set.seed(620)

res_mk <- hsim(h, size = 3000,

# for an illustration purpose

lambda_component0 = matrix(seq(1, 1.7, 0.1), nrow = 2))

res_mk

#> -------------------------------------------------------

#> Simulation result of exponential (marked) Hawkes model.

#> An object of class "hspec" of 2-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.02

#> [2,] 0.02

#>

#> Slot alpha:

#> [,1] [,2] [,3] [,4]

#> [1,] 3 2 0.3 0.2

#> [2,] 2 3 0.2 0.3

#>

#> Slot beta:

#> [,1] [,2] [,3] [,4]

#> [1,] 10 10 1 1

#> [2,] 10 10 1 1

#>

#> Slot type_col_map:

#> [[1]]

#> [1] 1 3

#>

#> [[2]]

#> [1] 2 4

#>

#>

#> Realized path :

#> arrival N1 N2 mark lambda1 lambda2 lambda11 lambda12 lambda13 lambda14

#> [1,] 0.0000 0 0 0 5.220 5.620 1.0000000 1.200e+00 1.4000 1.6000

#> [2,] 0.3339 1 0 1 2.247 2.397 0.0354893 4.259e-02 1.0026 1.1459

#> [3,] 1.2043 1 1 1 1.046 1.064 0.0005036 7.065e-06 0.5455 0.4799

#> [4,] 1.2103 2 1 1 3.122 4.182 0.0004743 1.884e+00 0.5423 0.6758

#> [5,] 1.3704 3 1 1 2.299 2.302 0.6051446 3.799e-01 0.7176 0.5758

#> [6,] 1.4098 3 2 1 4.238 3.474 2.4298143 2.561e-01 0.9783 0.5535

#> [7,] 1.5416 3 3 1 2.793 2.894 0.6507825 6.043e-01 0.8575 0.6605

#> [8,] 1.6639 3 4 1 2.498 2.919 0.1914158 7.660e-01 0.7588 0.7614

#> [9,] 2.0338 3 5 1 1.282 1.454 0.0047375 6.846e-02 0.5242 0.6642

#> [10,] 2.1098 4 5 1 2.276 2.981 0.0022151 9.671e-01 0.4858 0.8009

#> [11,] 2.3626 5 5 1 1.569 1.623 0.2396920 7.722e-02 0.6103 0.6220

#> [12,] 2.7052 5 6 1 1.216 1.178 0.1053725 2.511e-03 0.6462 0.4416

#> [13,] 2.7692 5 7 1 2.339 2.939 0.0555568 1.056e+00 0.6062 0.6018

#> [14,] 2.9333 6 7 1 1.818 2.272 0.0107638 5.920e-01 0.5144 0.6804

#> [15,] 3.0063 7 7 1 3.146 2.862 1.4508962 2.853e-01 0.7571 0.6325

#> [16,] 3.3222 7 8 1 1.453 1.365 0.1889842 1.211e-02 0.7707 0.4612

#> [17,] 3.3779 7 9 1 2.636 3.241 0.1082998 1.153e+00 0.7290 0.6254

#> [18,] 3.4084 8 9 1 3.931 5.226 0.0798097 2.324e+00 0.7071 0.8006

#> [19,] 3.7871 8 10 1 1.380 1.425 0.0698539 5.270e-02 0.6897 0.5482

#> [20,] 3.8329 9 10 1 2.736 3.505 0.0441702 1.298e+00 0.6588 0.7147

#> lambda21 lambda22 lambda23 lambda24

#> [1,] 1.1000000 1.300e+00 1.5000 1.7000

#> [2,] 0.0390382 4.614e-02 1.0742 1.2175

#> [3,] 0.0003383 7.654e-06 0.5336 0.5098

#> [4,] 0.0003186 2.826e+00 0.5304 0.8050

#> [5,] 0.4034302 5.699e-01 0.6224 0.6859

#> [6,] 1.6198765 3.841e-01 0.7906 0.6594

#> [7,] 0.4338551 9.064e-01 0.6930 0.8410

#> [8,] 0.1276106 1.149e+00 0.6132 1.0095

#> [9,] 0.0031583 1.027e-01 0.4236 0.9046

#> [10,] 0.0014767 1.451e+00 0.3926 1.1165

#> [11,] 0.1597947 1.158e-01 0.4602 0.8671

#> [12,] 0.0702484 3.767e-03 0.4687 0.6156

#> [13,] 0.0370378 1.584e+00 0.4397 0.8588

#> [14,] 0.0071759 8.881e-01 0.3731 0.9834

#> [15,] 0.9672641 4.280e-01 0.5328 0.9142

#> [16,] 0.1259895 1.817e-02 0.5343 0.6665

#> [17,] 0.0721999 1.730e+00 0.5053 0.9142

#> [18,] 0.0532064 3.485e+00 0.4901 1.1777

#> [19,] 0.0465693 7.905e-02 0.4726 0.8065

#> [20,] 0.0294468 1.947e+00 0.4514 1.0569

#> ... with 2980 more rows

#> -------------------------------------------------------

summary(hfit(h, res_mk$inter_arrival, res_mk$type,

lambda_component0 = matrix(seq(1, 1.7, 0.1), nrow = 2)))

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 69 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: 6084.702

#> 7 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.011596 0.007783 1.490 0.136238

#> alpha1.1 2.488160 0.242154 10.275 < 2e-16 ***

#> alpha1.2 1.354091 0.362072 3.740 0.000184 ***

#> alpha1.3 0.057595 0.096770 0.595 0.551729

#> alpha1.4 0.253495 0.115586 2.193 0.028298 *

#> beta1.1 6.383741 0.301811 21.151 < 2e-16 ***

#> beta1.3 0.755539 0.217985 3.466 0.000528 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------Synchronized intensity model

This model is basically two-kernel model and defined by little bit complicated reparameterization.

In order to handle complex re-parametrization, each slot is expressed

as a function rather than a matrix. The first argument

param is a set of parameters.

mu <- function(param = c(theta_p = 0.15, theta_n = 0.21, kappa = 0.12)){

theta <- (param["theta_n"] + param["theta_p"])/2

theta_tl <- (param["theta_n"] - param["theta_p"])/2

matrix(c(theta/2/(1 - param["kappa"]) + theta_tl/2/(1 + param["kappa"]),

theta/2/(1 - param["kappa"]) - theta_tl/2/(1 + param["kappa"])), nrow=2)

}

alpha <- function(param = c(eta = 5, nu = 3)){

zeta <- (param["eta"] + param["nu"])/2

zeta_tl <- (param["eta"] - param["nu"])/2

matrix(c(zeta, zeta_tl, zeta, -zeta_tl,

zeta, -zeta_tl, zeta, zeta_tl), nrow=2, byrow=TRUE)

}

beta <- function(param = c(beta = 12, kappa = 0.12)){

beta1 <- param["beta"] * (1 - param["kappa"])

beta2 <- param["beta"] * (1 + param["kappa"])

matrix(c(beta1, beta2, beta1, beta2,

beta1, beta2, beta1, beta2), nrow = 2, byrow = TRUE)

}

type_col_map <- list(c(1,2), c(3,4))

h_sy <- new("hspec", mu = mu, alpha = alpha, beta = beta, type_col_map = type_col_map)

h_sy

#> An object of class "hspec" of 2-dimensional Hawkes process

#>

#> Slot mu:

#> function (param = c(theta_p = 0.15, theta_n = 0.21, kappa = 0.12))

#> {

#> theta <- (param["theta_n"] + param["theta_p"])/2

#> theta_tl <- (param["theta_n"] - param["theta_p"])/2

#> matrix(c(theta/2/(1 - param["kappa"]) + theta_tl/2/(1 + param["kappa"]),

#> theta/2/(1 - param["kappa"]) - theta_tl/2/(1 + param["kappa"])),

#> nrow = 2)

#> }

#> <bytecode: 0x5641dc66b340>

#>

#> Slot alpha:

#> function (param = c(eta = 5, nu = 3))

#> {

#> zeta <- (param["eta"] + param["nu"])/2

#> zeta_tl <- (param["eta"] - param["nu"])/2

#> matrix(c(zeta, zeta_tl, zeta, -zeta_tl, zeta, -zeta_tl, zeta,

#> zeta_tl), nrow = 2, byrow = TRUE)

#> }

#> <bytecode: 0x5641dde947a8>

#>

#> Slot beta:

#> function (param = c(beta = 12, kappa = 0.12))

#> {

#> beta1 <- param["beta"] * (1 - param["kappa"])

#> beta2 <- param["beta"] * (1 + param["kappa"])

#> matrix(c(beta1, beta2, beta1, beta2, beta1, beta2, beta1,

#> beta2), nrow = 2, byrow = TRUE)

#> }

#> <bytecode: 0x5641dd73f4b0>

#>

#> Slot type_col_map:

#> [[1]]

#> [1] 1 2

#>

#> [[2]]

#> [1] 3 4

set.seed(1107)

# run simulation

res_sy <- hsim(h_sy, size = 2000, lambda_component0 = matrix(rep(1, 2 * 4), nrow=2))

summary(res_sy)

#> -------------------------------------------------------

#> Simulation result of exponential (marked) Hawkes model.

#> Realized path :

#> arrival N1 N2 mark lambda1 lambda2

#> [1,] 0.0000 0 0 0 4.11567 4.08888

#> [2,] 7.2506 0 1 1 0.11567 0.08888

#> [3,] 7.4805 0 2 1 0.42304 0.48724

#> [4,] 7.4915 1 2 1 3.09049 4.86829

#> [5,] 17.7981 2 2 1 0.11567 0.08888

#> [6,] 20.0276 2 3 1 0.11567 0.08888

#> [7,] 20.0484 2 4 1 2.56966 4.05419

#> [8,] 20.0609 3 4 1 4.94847 7.88899

#> [9,] 20.1607 4 4 1 3.58697 3.81330

#> [10,] 20.2304 5 4 1 4.09539 3.38445

#> [11,] 20.5057 5 5 1 0.56602 0.47289

#> [12,] 26.4862 6 5 1 0.11567 0.08888

#> [13,] 32.5114 6 6 1 0.11567 0.08888

#> [14,] 32.6227 6 7 1 1.12663 1.54804

#> [15,] 32.6316 6 8 1 3.79509 5.94053

#> [16,] 32.6480 7 8 1 5.81283 9.13210

#> [17,] 32.6921 7 9 1 6.87877 7.59586

#> [18,] 32.7953 8 9 1 3.51752 4.17621

#> [19,] 32.9249 8 10 1 2.20298 1.94570

#> [20,] 34.7648 9 10 1 0.11567 0.08888

#> ... with 1980 more rows

#> -------------------------------------------------------The estimation is based on function arguments param. In

addition, the initial values of the numerical optimization is the

default values specified in param. Note that the same name

arguments are treated as the same parameter. kappa is in

both of mu and beta, but only one

kappa appears in the estimation result.

fit_sy <- hfit(h_sy, inter_arrival=res_sy$inter_arrival,

type=res_sy$type,

lambda_component0 = matrix(rep(1, 2 * 4), nrow=2))

summary(fit_sy)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 77 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -260.6273

#> 6 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> theta_p 0.08291 0.01587 5.223 1.76e-07 ***

#> theta_n 0.16264 0.01695 9.594 < 2e-16 ***

#> kappa 0.40990 0.02294 17.866 < 2e-16 ***

#> eta 5.23253 0.36946 14.163 < 2e-16 ***

#> nu 2.89429 0.32969 8.779 < 2e-16 ***

#> beta 18.01820 NaN NaN NaN

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------Extended model

The following family of extended multi-variate marked Hawkes models are implemented:

where the kernel is represented by

and

is a constant matrix,

is additional impacts on intensities, which may depend on mark, or any information generated by underlying processes,

is exponential decaying matrix such that ,

denotes the random measures defined on the product of time and mark spaces.

Linear impact model

In the linear impact model,

impact represents

,

the impact of mark on future intensity. For details, see Marked

Hawkes process modeling of price dynamics and volatility

estimation.

It is a function, and the first argument is param

represents the parameter of the model. impact() function

can have additional arguments related to the model specification or

generated path, such as n, mark, etc. Do not

miss ... as the ellipsis is omitted, an error occurs.

rmark() is a function that generate marks for

simulation.

mu <- matrix(c(0.15, 0.15), nrow=2)

alpha <- matrix(c(0.75, 0.6, 0.6, 0.75), nrow=2, byrow=T)

beta <- matrix(c(2.6, 2.6, 2.6, 2.6), nrow=2)

rmark <- function(param = c(p=0.65), ...){

rgeom(1, p=param[1]) + 1

}

impact <- function(param = c(eta1=0.2), alpha, n, mark, ...){

ma <- matrix(rep(mark[n]-1, 4), nrow = 2)

ma * matrix( rep(param["eta1"], 4), nrow=2)

}

hi <- new("hspec", mu=mu, alpha=alpha, beta=beta,

rmark = rmark,

impact=impact)

hi

#> An object of class "hspec" of 2-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.15

#> [2,] 0.15

#>

#> Slot alpha:

#> [,1] [,2]

#> [1,] 0.75 0.60

#> [2,] 0.60 0.75

#>

#> Slot beta:

#> [,1] [,2]

#> [1,] 2.6 2.6

#> [2,] 2.6 2.6

#>

#> Slot impact:

#> function (param = c(eta1 = 0.2), alpha, n, mark, ...)

#> {

#> ma <- matrix(rep(mark[n] - 1, 4), nrow = 2)

#> ma * matrix(rep(param["eta1"], 4), nrow = 2)

#> }

#>

#> Slot rmark:

#> function (param = c(p = 0.65), ...)

#> {

#> rgeom(1, p = param[1]) + 1

#> }

set.seed(1107)

res_impact <- hsim(hi, size=1000, lambda_component0 = matrix(rep(0.1,4), nrow=2))

summary(res_impact)

#> -------------------------------------------------------

#> Simulation result of exponential (marked) Hawkes model.

#> Realized path :

#> arrival N1 N2 mark lambda1 lambda2

#> [1,] 0.0000 0 0 0 0.35000 0.35000

#> [2,] 1.3001 0 1 1 0.15681 0.15681

#> [3,] 2.5585 1 1 2 0.17302 0.17871

#> [4,] 2.7982 1 2 1 0.67171 0.59433

#> [5,] 3.0525 2 2 2 0.72904 0.76653

#> [6,] 3.3929 3 2 1 0.78108 0.73464

#> [7,] 3.4509 4 2 3 1.33764 1.16872

#> [8,] 3.5101 5 2 2 2.15429 1.88085

#> [9,] 3.5837 6 2 1 2.58987 2.24016

#> [10,] 3.6041 7 2 1 3.17455 2.70074

#> [11,] 3.7053 8 2 1 3.05159 2.57205

#> [12,] 3.9277 9 2 1 2.19788 1.84482

#> [13,] 3.9610 10 2 1 2.71584 2.25450

#> [14,] 4.2448 11 2 1 1.73576 1.44339

#> [15,] 4.7277 12 2 4 0.81551 0.68947

#> [16,] 5.1473 12 3 1 0.82698 0.73426

#> [17,] 5.3229 12 4 2 0.95877 0.99505

#> [18,] 5.4219 13 4 1 1.39371 1.53772

#> [19,] 5.4869 14 4 2 1.83388 1.82882

#> [20,] 5.8857 14 5 1 1.08385 1.02887

#> ... with 980 more rows

#> -------------------------------------------------------

fit <- hfit(hi,

inter_arrival = res_impact$inter_arrival,

type = res_impact$type,

mark = res_impact$mark,

lambda_component0 = matrix(rep(0.1,4), nrow=2))

summary(fit)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 38 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -1525.501

#> 5 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.13190 0.00891 14.804 <2e-16 ***

#> alpha1.1 0.67609 0.07742 8.732 <2e-16 ***

#> alpha1.2 0.60345 0.07211 8.368 <2e-16 ***

#> beta1.1 2.22126 0.16730 13.277 <2e-16 ***

#> eta1 0.11635 0.05549 2.097 0.036 *

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------For a special case of linear impact function, the following

implementation is recommended. In a marked Hawkes model, the additional

linear impact can be represented by slot eta. In this

model, the intensity process is

rmark <- function(param = c(p=0.65), ...){

rgeom(1, p=param[1]) + 1

}

h <- new("hspec", mu=0.15, alpha=0.7, beta=1.6, eta=0.3,

rmark = rmark)

h

#> An object of class "hspec" of 1-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.15

#>

#> Slot alpha:

#> [,1]

#> [1,] 0.7

#>

#> Slot beta:

#> [,1]

#> [1,] 1.6

#>

#> Slot eta:

#> [,1]

#> [1,] 0.3

#>

#> Slot rmark:

#> function (param = c(p = 0.65), ...)

#> {

#> rgeom(1, p = param[1]) + 1

#> }

set.seed(1107)

res <- hsim(h, size = 1000)

summary(res)

#> -------------------------------------------------------

#> Simulation result of exponential (marked) Hawkes model.

#> Realized path :

#> arrival N1 mark lambda1

#> [1,] 0.0000 0 0 0.20833

#> [2,] 1.9559 1 1 0.15255

#> [3,] 3.2143 2 1 0.24381

#> [4,] 3.9750 3 1 0.38501

#> [5,] 4.5731 4 1 0.50912

#> [6,] 7.7740 5 1 0.15632

#> [7,] 11.9290 6 2 0.15092

#> [8,] 13.4270 7 1 0.24108

#> [9,] 23.3482 8 1 0.15000

#> [10,] 31.9666 9 3 0.15000

#> [11,] 32.0257 10 2 1.33257

#> [12,] 32.1598 11 1 1.91124

#> [13,] 36.9851 12 1 0.15109

#> [14,] 37.1167 13 2 0.71795

#> [15,] 38.4261 14 1 0.34298

#> [16,] 38.9803 15 1 0.51792

#> [17,] 42.9827 16 2 0.15177

#> [18,] 48.4580 17 1 0.15016

#> [19,] 48.7737 18 1 0.57247

#> [20,] 48.7910 19 2 1.24194

#> ... with 980 more rows

#> -------------------------------------------------------

fit <- hfit(h,

inter_arrival = res$inter_arrival,

type = res$type,

mark = res$mark)

summary(fit)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 37 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -1684.238

#> 4 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.14557 0.00847 17.187 < 2e-16 ***

#> alpha1 0.63917 0.06892 9.275 < 2e-16 ***

#> beta1 1.48983 0.12320 12.092 < 2e-16 ***

#> eta1 0.33626 0.07723 4.354 1.34e-05 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------If you want to estimate the mark distribution also, then

dmark slot that describes the density function of mark is

required.

h_md <- h

h_md@dmark <- function(param = c(p = 0.1), n=n, mark=mark, ...){

dgeom(mark[n] - 1, prob = param["p"])

}

mle_md <- hfit(h_md,

inter_arrival = res$inter_arrival, type = res$type, mark = res$mark)

summary(mle_md)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 46 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -2657.079

#> 5 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.145574 0.008468 17.190 < 2e-16 ***

#> alpha1 0.639168 0.069753 9.163 < 2e-16 ***

#> beta1 1.489843 0.124301 11.986 < 2e-16 ***

#> eta1 0.336259 0.076904 4.372 1.23e-05 ***

#> p 0.658970 0.012203 54.002 < 2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------Hawkes flocking model

The function is not necessarily depend on mark. In the Hawkes flocking model, the kernel component is represented by

where

For details, see Systemic risk in market microstructure of crude oil and gasoline futures prices: A Hawkes flocking model approach.

In the basic model, alpha is a matrix, but it can be a

function as in the following code. The function alpha

simply return a

matrix but by doing so, we can fix some of elements as specific vales

when estimating. When estimating, the optimization is only applied for

the specified parameters in the argument param. In the case

of simulation, there is no difference whether the parameter set is

represented by a matrix or a function.

mu <- matrix(c(0.02, 0.02, 0.04, 0.04), nrow = 4)

alpha <- function(param = c(alpha11 = 0.2, alpha12 = 0.3, alpha33 = 0.3, alpha34 = 0.4)){

matrix(c(param["alpha11"], param["alpha12"], 0, 0,

param["alpha12"], param["alpha11"], 0, 0,

0, 0, param["alpha33"], param["alpha34"],

0, 0, param["alpha34"], param["alpha33"]), nrow = 4, byrow = TRUE)

}

beta <- matrix(c(rep(0.7, 8), rep(1.1, 8)), nrow = 4, byrow = TRUE)impact() function is little bit complicated, but it is

nothing more than expressing the definition of the model to an R

function. Note that we specify N=N, n=n in the argument.

N is for counting process

and n denotes the time step. Both are needed to implement

the function body and it is required to specify in the argument.

… also should not be omitted.

impact <- function(param = c(alpha1n=0.25, alpha1w=0.1, alpha2n=0.1, alpha2w=0.2),

N=N, n=n, ...){

Psi <- matrix(c(0, 0, param['alpha1w'], param['alpha1n'],

0, 0, param['alpha1n'], param['alpha1w'],

param['alpha2w'], param['alpha2n'], 0, 0,

param['alpha2n'], param['alpha2w'], 0, 0), nrow=4, byrow=TRUE)

ind <- N[,"N1"][n] - N[,"N2"][n] > N[,"N3"][n] - N[,"N4"][n]

km <- matrix(c(!ind, !ind, !ind, !ind,

ind, ind, ind, ind,

ind, ind, ind, ind,

!ind, !ind, !ind, !ind), nrow = 4, byrow = TRUE)

km * Psi

}

hspec_fl <- new("hspec",

mu = mu, alpha = alpha, beta = beta, impact = impact)

hspec_fl

#> An object of class "hspec" of 4-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.02

#> [2,] 0.02

#> [3,] 0.04

#> [4,] 0.04

#>

#> Slot alpha:

#> function (param = c(alpha11 = 0.2, alpha12 = 0.3, alpha33 = 0.3,

#> alpha34 = 0.4))

#> {

#> matrix(c(param["alpha11"], param["alpha12"], 0, 0, param["alpha12"],

#> param["alpha11"], 0, 0, 0, 0, param["alpha33"], param["alpha34"],

#> 0, 0, param["alpha34"], param["alpha33"]), nrow = 4,

#> byrow = TRUE)

#> }

#> <bytecode: 0x5641dca01638>

#>

#> Slot beta:

#> [,1] [,2] [,3] [,4]

#> [1,] 0.7 0.7 0.7 0.7

#> [2,] 0.7 0.7 0.7 0.7

#> [3,] 1.1 1.1 1.1 1.1

#> [4,] 1.1 1.1 1.1 1.1

#>

#> Slot impact:

#> function (param = c(alpha1n = 0.25, alpha1w = 0.1, alpha2n = 0.1,

#> alpha2w = 0.2), N = N, n = n, ...)

#> {

#> Psi <- matrix(c(0, 0, param["alpha1w"], param["alpha1n"],

#> 0, 0, param["alpha1n"], param["alpha1w"], param["alpha2w"],

#> param["alpha2n"], 0, 0, param["alpha2n"], param["alpha2w"],

#> 0, 0), nrow = 4, byrow = TRUE)

#> ind <- N[, "N1"][n] - N[, "N2"][n] > N[, "N3"][n] - N[, "N4"][n]

#> km <- matrix(c(!ind, !ind, !ind, !ind, ind, ind, ind, ind,

#> ind, ind, ind, ind, !ind, !ind, !ind, !ind), nrow = 4,

#> byrow = TRUE)

#> km * Psi

#> }

set.seed(1107)

hr_fl <- hsim(hspec_fl, size=2000)

summary(hr_fl)

#> -------------------------------------------------------

#> Simulation result of exponential (marked) Hawkes model.

#> Realized path :

#> arrival N1 N2 N3 N4 mark lambda1 lambda2 lambda3 lambda4

#> [1,] 0.00000 0 0 0 0 0 0.070000 0.070000 0.110000 0.110000

#> [2,] 0.84055 0 0 1 0 1 0.047761 0.047761 0.067768 0.067768

#> [3,] 7.35095 0 0 2 0 1 0.021340 0.020291 0.040254 0.040332

#> [4,] 8.74603 1 0 2 0 1 0.058165 0.020110 0.104718 0.126289

#> [5,] 29.54186 2 0 2 0 1 0.020000 0.020000 0.040000 0.040000

#> [6,] 30.90333 2 1 2 0 1 0.097114 0.135671 0.040000 0.062366

#> [7,] 31.08275 3 1 2 0 1 0.352605 0.298414 0.040000 0.222539

#> [8,] 33.42583 4 1 2 0 1 0.123299 0.132184 0.040000 0.061465

#> [9,] 33.75532 5 1 2 0 1 0.260826 0.347283 0.179195 0.054939

#> [10,] 34.28018 6 1 2 0 1 0.325287 0.454414 0.230420 0.048387

#> [11,] 35.06698 6 2 2 0 1 0.311303 0.443397 0.204307 0.043530

#> [12,] 35.31209 6 3 2 0 1 0.518076 0.545110 0.241844 0.042695

#> [13,] 35.91748 6 4 2 0 1 0.542398 0.494637 0.195086 0.041385

#> [14,] 36.30025 7 4 2 0 1 0.649096 0.536065 0.141792 0.172180

#> [15,] 36.96094 7 5 2 0 1 0.542096 0.533891 0.185908 0.103906

#> [16,] 36.99520 7 5 2 1 1 0.822615 0.716974 0.180512 0.294145

#> [17,] 37.01805 8 5 2 1 1 0.809878 0.804326 0.567094 0.580389

#> [18,] 37.57785 9 5 2 1 1 0.688962 0.752790 0.432793 0.331931

#> [19,] 39.12437 9 5 2 2 1 0.314339 0.369832 0.148166 0.093268

#> [20,] 40.15404 10 5 2 2 1 0.163160 0.238789 0.203723 0.153817

#> ... with 1980 more rows

#> -------------------------------------------------------

fit_fl <- hfit(hspec_fl, hr_fl$inter_arrival, hr_fl$type)

summary(fit_fl)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 84 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -3050.319

#> 12 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.028055 0.004311 6.509 7.59e-11 ***

#> mu3 0.033179 0.004284 7.745 9.53e-15 ***

#> alpha11 0.199720 0.029151 6.851 7.32e-12 ***

#> alpha12 0.312236 0.030731 10.160 < 2e-16 ***

#> alpha33 0.283861 0.037992 7.472 7.93e-14 ***

#> alpha34 0.341250 0.041153 8.292 < 2e-16 ***

#> beta1.1 0.734703 0.054270 13.538 < 2e-16 ***

#> beta3.1 0.899924 0.081923 10.985 < 2e-16 ***

#> alpha1n 0.250338 0.044096 5.677 1.37e-08 ***

#> alpha1w 0.107483 0.030036 3.579 0.000346 ***

#> alpha2n 0.083683 0.038739 2.160 0.030761 *

#> alpha2w 0.172788 0.034234 5.047 4.48e-07 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------Bid-ask price model

In this model, we use a system of counting processes with the corresponding conditional intensities to describe the bid-ask price processes:

The ask price process and the bid price process is . The mid price process is plus initial mid price level.

The base intensity process is

where is the absolute level of the bid-ask spread with implying the minimum level. For details, see Modeling bid and ask price dynamics with an extended Hawkes process and its empirical applications for high-frequency stock market data.

Note that in the following code of the definition of mu,

n is needed to represent time

and Nc is needed to calculate the level and mid price.

# presumed initial bid and ask prices

initial_ask_price <- 1250 #cents

initial_bid_price <- 1150 #cents

initial_level <- round((initial_ask_price - initial_bid_price) - 1)

initial_mid_price <- (initial_bid_price + initial_ask_price) / 2

mu <- function(param = c(mu1 = 0.08, zeta1 = 0.10), n=n, Nc=Nc, ...){

if(n == 1){

level <- initial_level

mid <- initial_mid_price

} else {

level <- Nc[n-1,1] - Nc[n-1,2] - (Nc[n-1,3] - Nc[n-1,4]) + initial_level

ask <- initial_ask_price + (Nc[n-1,1] - Nc[n-1,2])

bid <- initial_bid_price + (Nc[n-1,3] - Nc[n-1,4])

mid <- (ask + bid) / 2

}

if(level <= 0){

matrix(c(param["mu1"], 0,

0, param["mu1"]), nrow = 4)

} else {

matrix(c(param["mu1"], param["zeta1"] * level / mid,

param["zeta1"]*level / mid, param["mu1"]), nrow = 4)

}

}In addition, the kernel is represented by

where

for constant and is a component of such that

In the following code, we separate the constant part of

as alpha and stochastic part as impact. To

represent

,

we need lambda_component. Note that

alpha <- function(param = c(alpha_s1=4, alpha_m=26, alpha_s2=5,

alpha_w1=11, alpha_w2=7)){

matrix(c(param["alpha_s1"], param["alpha_m"], param["alpha_s2"], 0,

param["alpha_w1"], 0, 0, param["alpha_w2"],

param["alpha_w2"], 0, 0, param["alpha_w1"],

0, param["alpha_s2"], param["alpha_m"], param["alpha_s1"]), nrow = 4, byrow = TRUE)

}

impact <- function(param = c(xi = 2.7), n=n, Nc=Nc, lambda_component = lambda_component, ... ){

if(n == 1){

level <- initial_level

# mid <- initial_mid_price

} else {

level <- Nc[n,1] - Nc[n,2] - (Nc[n,3] - Nc[n,4]) + initial_level

ask <- initial_ask_price + (Nc[n,1] - Nc[n,2])

bid <- initial_bid_price + (Nc[n,3] - Nc[n,4])

mid <- (ask + bid)/2

}

lambda_component_matrix <- matrix(lambda_component[n, ], nrow=4, byrow=TRUE)

l2 <- sum(lambda_component_matrix[2,]) # sum of second row

l3 <- sum(lambda_component_matrix[3,]) # sum of third row

im <- matrix(c(0, 0, 0, 0,

0, -l2 + param["xi"]*level/mid, -l2 + param["xi"]*level/mid, 0,

0, -l3 + param["xi"]*level/mid, -l3 + param["xi"]*level/mid, 0,

0, 0, 0, 0), nrow = 4, byrow = TRUE)

}

beta <- matrix(rep(50, 16), nrow = 4, byrow=TRUE)

rmark <- function(n=n, Nc=Nc, type, ...){

if(n == 1){

level <- initial_level

} else {

level <- Nc[n-1,1] - Nc[n-1,2] - (Nc[n-1,3] - Nc[n-1,4]) + initial_level

}

if (type[n] == 2 | type[n] == 3){

min(level, rgeom(1, p=0.65) + 1)

} else {

rgeom(1, p=0.65) + 1

}

}

h_ba <- new("hspec", mu = mu, alpha = alpha, beta = beta, impact=impact, rmark = rmark)

h_ba

#> An object of class "hspec" of 4-dimensional Hawkes process

#>

#> Slot mu:

#> function (param = c(mu1 = 0.08, zeta1 = 0.1), n = n, Nc = Nc,

#> ...)

#> {

#> if (n == 1) {

#> level <- initial_level

#> mid <- initial_mid_price

#> }

#> else {

#> level <- Nc[n - 1, 1] - Nc[n - 1, 2] - (Nc[n - 1, 3] -

#> Nc[n - 1, 4]) + initial_level

#> ask <- initial_ask_price + (Nc[n - 1, 1] - Nc[n - 1,

#> 2])

#> bid <- initial_bid_price + (Nc[n - 1, 3] - Nc[n - 1,

#> 4])

#> mid <- (ask + bid)/2

#> }

#> if (level <= 0) {

#> matrix(c(param["mu1"], 0, 0, param["mu1"]), nrow = 4)

#> }

#> else {

#> matrix(c(param["mu1"], param["zeta1"] * level/mid, param["zeta1"] *

#> level/mid, param["mu1"]), nrow = 4)

#> }

#> }

#>

#> Slot alpha:

#> function (param = c(alpha_s1 = 4, alpha_m = 26, alpha_s2 = 5,

#> alpha_w1 = 11, alpha_w2 = 7))

#> {

#> matrix(c(param["alpha_s1"], param["alpha_m"], param["alpha_s2"],

#> 0, param["alpha_w1"], 0, 0, param["alpha_w2"], param["alpha_w2"],

#> 0, 0, param["alpha_w1"], 0, param["alpha_s2"], param["alpha_m"],

#> param["alpha_s1"]), nrow = 4, byrow = TRUE)

#> }

#> <bytecode: 0x5641dabe9ce0>

#>

#> Slot beta:

#> [,1] [,2] [,3] [,4]

#> [1,] 50 50 50 50

#> [2,] 50 50 50 50

#> [3,] 50 50 50 50

#> [4,] 50 50 50 50

#>

#> Slot impact:

#> function (param = c(xi = 2.7), n = n, Nc = Nc, lambda_component = lambda_component,

#> ...)

#> {

#> if (n == 1) {

#> level <- initial_level

#> }

#> else {

#> level <- Nc[n, 1] - Nc[n, 2] - (Nc[n, 3] - Nc[n, 4]) +

#> initial_level

#> ask <- initial_ask_price + (Nc[n, 1] - Nc[n, 2])

#> bid <- initial_bid_price + (Nc[n, 3] - Nc[n, 4])

#> mid <- (ask + bid)/2

#> }

#> lambda_component_matrix <- matrix(lambda_component[n, ],

#> nrow = 4, byrow = TRUE)

#> l2 <- sum(lambda_component_matrix[2, ])

#> l3 <- sum(lambda_component_matrix[3, ])

#> im <- matrix(c(0, 0, 0, 0, 0, -l2 + param["xi"] * level/mid,

#> -l2 + param["xi"] * level/mid, 0, 0, -l3 + param["xi"] *

#> level/mid, -l3 + param["xi"] * level/mid, 0, 0, 0,

#> 0, 0), nrow = 4, byrow = TRUE)

#> }

#>

#> Slot rmark:

#> function (n = n, Nc = Nc, type, ...)

#> {

#> if (n == 1) {

#> level <- initial_level

#> }

#> else {

#> level <- Nc[n - 1, 1] - Nc[n - 1, 2] - (Nc[n - 1, 3] -

#> Nc[n - 1, 4]) + initial_level

#> }

#> if (type[n] == 2 | type[n] == 3) {

#> min(level, rgeom(1, p = 0.65) + 1)

#> }

#> else {

#> rgeom(1, p = 0.65) + 1

#> }

#> }

set.seed(1107)

hr_ba <- hsim(h_ba, size=1000, lambda_component0 = matrix(rep(1, 16), 4))

summary(hr_ba)

#> -------------------------------------------------------

#> Simulation result of exponential (marked) Hawkes model.

#> Realized path :

#> arrival N1 N2 N3 N4 mark lambda1 lambda2 lambda3 lambda4

#> [1,] 0.0000 0 0 0 0 0 4.08000 4.0082500 4.0082500 4.0800

#> [2,] 3.6673 1 0 0 0 2 0.08000 0.0082500 0.0082500 0.0800

#> [3,] 6.9225 2 0 0 0 1 0.08000 0.0084097 0.0084097 0.0800

#> [4,] 20.0251 2 0 0 1 1 0.08000 0.0084894 0.0084894 0.0800

#> [5,] 24.3957 2 0 0 2 3 0.08000 0.0085762 0.0085762 0.0800

#> [6,] 24.4026 2 0 1 2 1 0.08000 4.9856950 7.8296138 2.9239

#> [7,] 27.9067 3 0 1 2 1 0.08000 0.0087500 0.0087500 0.0800

#> [8,] 27.9378 3 1 1 2 1 0.92442 2.3309869 1.4865661 0.0800

#> [9,] 33.8868 3 1 2 2 2 0.08000 0.0087500 0.0087500 0.0800

#> [10,] 33.8900 3 1 2 3 1 4.33027 0.2054120 0.2054120 22.1814

#> [11,] 34.3764 4 1 2 3 1 0.08000 0.0086631 0.0086631 0.0800

#> [12,] 34.4342 4 2 2 3 1 0.30328 0.6227650 0.3994842 0.0800

#> [13,] 36.5641 5 2 2 3 2 0.08000 0.0086631 0.0086631 0.0800

#> [14,] 36.5658 5 3 2 3 2 3.74917 10.0990280 6.4298623 0.0800

#> [15,] 40.4590 5 3 2 4 1 0.08000 0.0086631 0.0086631 0.0800

#> [16,] 40.4666 5 3 3 4 1 0.08000 4.8059475 7.5472032 2.8213

#> [17,] 43.8835 6 3 3 4 5 0.08000 0.0086631 0.0086631 0.0800

#> [18,] 44.8818 7 3 3 4 2 0.08000 0.0090607 0.0090607 0.0800

#> [19,] 47.6976 7 3 3 5 2 0.08000 0.0092193 0.0092193 0.0800

#> [20,] 51.7138 8 3 3 5 1 0.08000 0.0093932 0.0093932 0.0800

#> ... with 980 more rows

#> -------------------------------------------------------As a separate log-likelihood estimation performed, the parameter for mark distribution is not estimated.

logLik(h_ba, inter_arrival = hr_ba$inter_arrival, type = hr_ba$type, Nc = hr_ba$Nc,

lambda_component0 = matrix(rep(1, 16), 4))

#> loglikelihood

#> -1817.794

mle_ba <- hfit(h_ba, inter_arrival = hr_ba$inter_arrival, type = hr_ba$type,

lambda_component0 = matrix(rep(1, 16), 4))

summary(mle_ba)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 37 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -1810.43

#> 9 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.069541 0.003583 19.407 < 2e-16 ***

#> zeta1 0.135214 0.010696 12.641 < 2e-16 ***

#> alpha_s1 4.656127 1.091747 4.265 2e-05 ***

#> alpha_m 23.554240 NaN NaN NaN

#> alpha_s2 5.849631 6.305055 0.928 0.353528

#> alpha_w1 10.283690 2.860066 3.596 0.000324 ***

#> alpha_w2 7.402715 2.299566 3.219 0.001286 **

#> beta1.1 51.868593 3.094326 16.762 < 2e-16 ***

#> xi 2.376550 NaN NaN NaN

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#> --------------------------------------------Point process with flexible residual

One-dimensional model

This code demonstrates how to create a point process with a flexible

residual structure. For details, see Self

and mutually exciting point process embedding flexible residuals and

intensity with discretely Markovian dynamics. The distribution used

in this example is a combination of a trapezoid and an exponential

distribution. The dresidual and presidual

functions receive their necessary parameters bundled into a param

vector. In the context of a Hawkes process model, these functions

correspond to the case where the residuals are unit exponential

distributions.

mu1_d <- 0.5; alpha1_d <- 1; beta1_d <- 1.2; a <- 0.7; ell <- 1.6

hspec1_d <- new("hspec", mu=mu1_d, alpha=alpha1_d, beta=beta1_d,

rresidual = function(size) rtzexp(n=size, a = a, ell = ell),

dresidual = function(x, param = c(a = a, ell = ell))

dtzexp(x, a = param["a"], ell = param["ell"]),

presidual = function(q, param = c(a = a, ell = ell))

ptzexp(q, a = param["a"], ell = param["ell"]),

qresidual = function(p, param = c(a = a, ell = ell))

qtzexp(p, a = param["a"], ell = param["ell"]))

dh1_real <- hsim(hspec1_d, size = 3000)

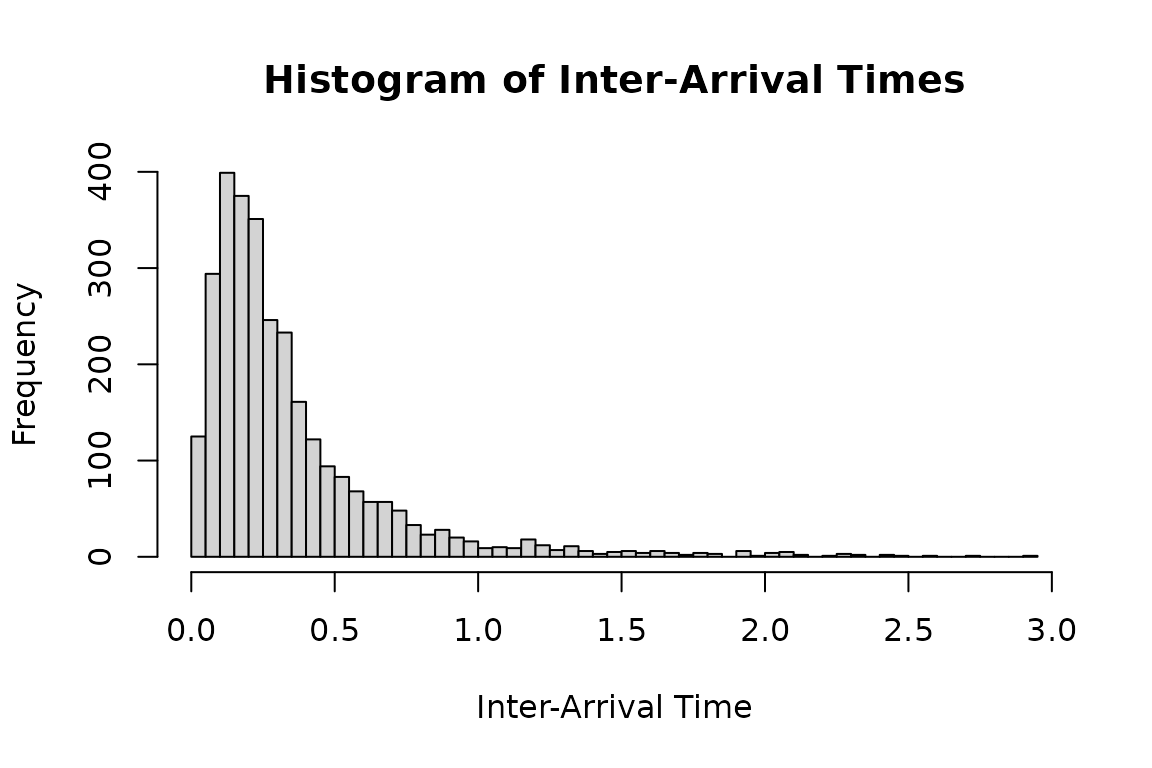

hist(

dh1_real$inter_arrival[dh1_real$inter_arrival < 3],

breaks = 50,

main = "Histogram of Inter-Arrival Times",

xlab = "Inter-Arrival Time",

ylab = "Frequency"

)

This R code snippet demonstrates how to analyze the residual process

of a point process model using a flexible distribution. The logLik

function is used to compute the log-likelihood of observed inter-arrival

times (dh1_real$inter_arrival) based on the distribution

specified by hspec1_d. The infer = TRUE

parameter allows the function to also infer the residual process,

storing the results in infer_res_dh1.

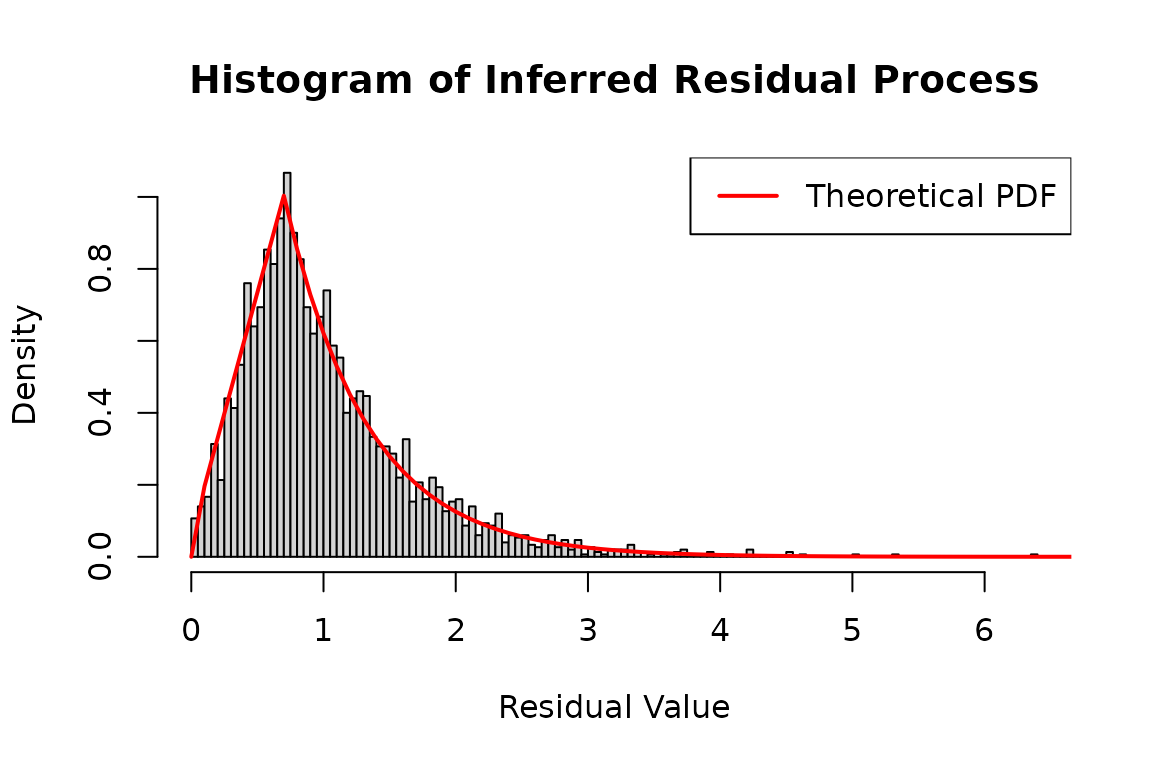

# Infer the residual process using the log-likelihood method

# 'infer_res_dh1' contains the inferred process data based on the inter-arrival times

infer_res_dh1 <- logLik(hspec1_d, inter_arrival = dh1_real$inter_arrival, infer = TRUE)

# Plot a histogram of the inferred residual process

hist(

infer_res_dh1$res_process1,

breaks = 100,

probability = TRUE,

main = "Histogram of Inferred Residual Process",

xlab = "Residual Value",

ylab = "Density"

)

x <- seq(0, 8, 0.1)

lines(

x,

dtzexp(x, a = a, ell = ell),

col = 'red',

lwd = 2

)

# Add legend for clarity

legend("topright", legend = "Theoretical PDF", col = "red", lwd = 2)

Two-dimenional model

The above method can be extended to multi-dimensions. The basic approach to extension is similar to how multi-dimensional Hawkes models are handled.

mu2_d <- matrix(c(0.3), nrow = 2)

alpha2_d <- matrix(c(0.5, 0.8, 0.8, 0.5), nrow = 2, byrow = TRUE)

beta2_d <- matrix(c(1.5, 1.5, 1.5, 1.5), nrow = 2, byrow = TRUE)

a <- 0.7; ell <- 1.6

hspec2_du <- new("hspec", mu=mu2_d, alpha=alpha2_d, beta=beta2_d,

rresidual = function(size) rtzexp(n=size, a = a, ell = ell),

dresidual = function(x, param = c(a = a, ell = ell))

dtzexp(x, a = param["a"], ell = param["ell"]),

presidual = function(q, param = c(a = a, ell = ell))

ptzexp(q, a = param["a"], ell = param["ell"]),

qresidual = function(p, param = c(a = a, ell = ell))

qtzexp(p, a = param["a"], ell = param["ell"]))

print(hspec2_du)

#> An object of class "hspec" of 2-dimensional Hawkes process

#>

#> Slot mu:

#> [,1]

#> [1,] 0.3

#> [2,] 0.3

#>

#> Slot alpha:

#> [,1] [,2]

#> [1,] 0.5 0.8

#> [2,] 0.8 0.5

#>

#> Slot beta:

#> [,1] [,2]

#> [1,] 1.5 1.5

#> [2,] 1.5 1.5

#>

#> Slot rresidual:

#> function (size)

#> rtzexp(n = size, a = a, ell = ell)

#>

#> Slot dresidual:

#> function (x, param = c(a = a, ell = ell))

#> dtzexp(x, a = param["a"], ell = param["ell"])

#>

#> Slot presidual:

#> function (q, param = c(a = a, ell = ell))

#> ptzexp(q, a = param["a"], ell = param["ell"])

#>

#> Slot qresidual:

#> function (p, param = c(a = a, ell = ell))

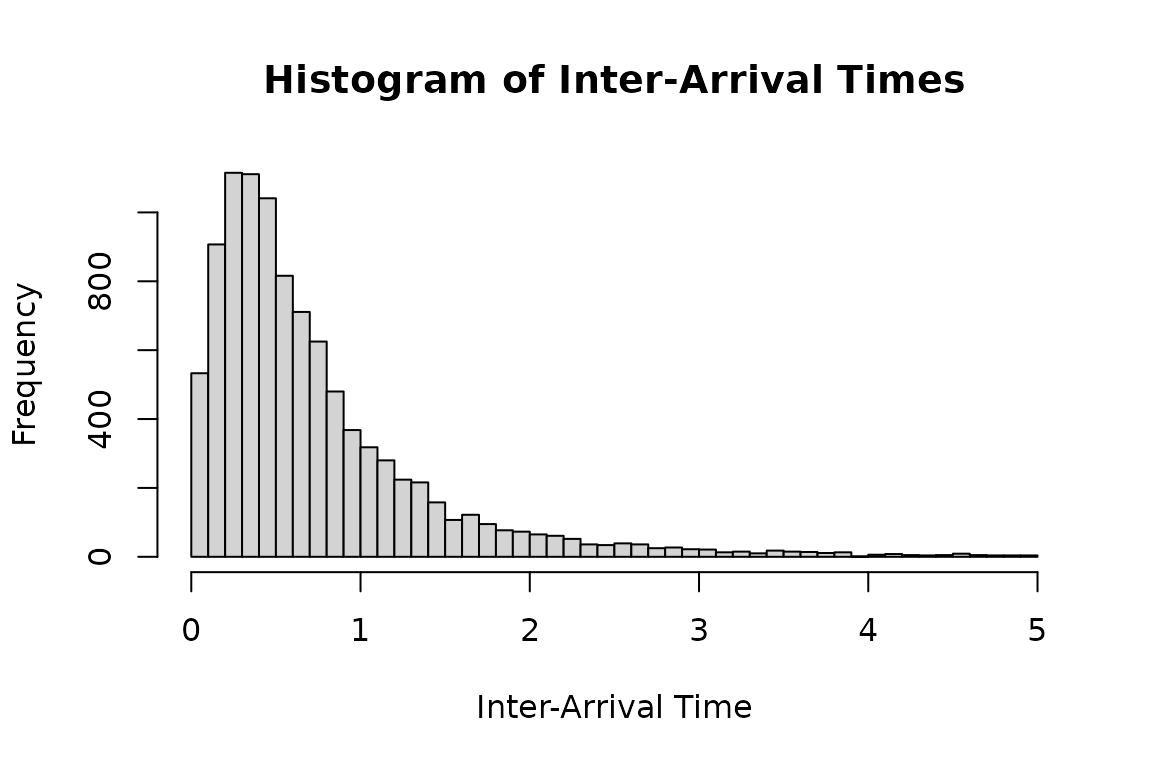

#> qtzexp(p, a = param["a"], ell = param["ell"])Histogram of inter-arrival times under tzexp

distribution.

set.seed(1107)

duh2_real <- hsim(hspec2_du, size = 10000)

# Plot a histogram of the inter-arrival times less than 5

hist(

duh2_real$inter_arrival[duh2_real$inter_arrival < 5],

breaks = 50,

main = "Histogram of Inter-Arrival Times",

xlab = "Inter-Arrival Time",

ylab = "Frequency"

)

Inference based on the flexible residual model.

infer_res_dh2 <- logLik(hspec2_du,

inter_arrival = duh2_real$inter_arrival,

type = duh2_real$type, infer = TRUE)The residual process follows the residual distribution in the model.

# Plot a histogram of the inferred residual process

hist(

infer_res_dh2$res_process2,

breaks = 50,

probability = TRUE,

main = "Histogram of Inferred Residual Process",

xlab = "Residual Value",

ylab = "Density"

)

# Generate a sequence of x values for plotting the theoretical distribution

x <- seq(0, 8, 0.1)

# Add a line to the histogram representing the theoretical density function

lines(

x,

dtzexp(x, a = a, ell = ell),

col = 'red',

lwd = 2

)

# Add legend for clarity

legend("topright", legend = "Theoretical PDF", col = "red", lwd = 2)

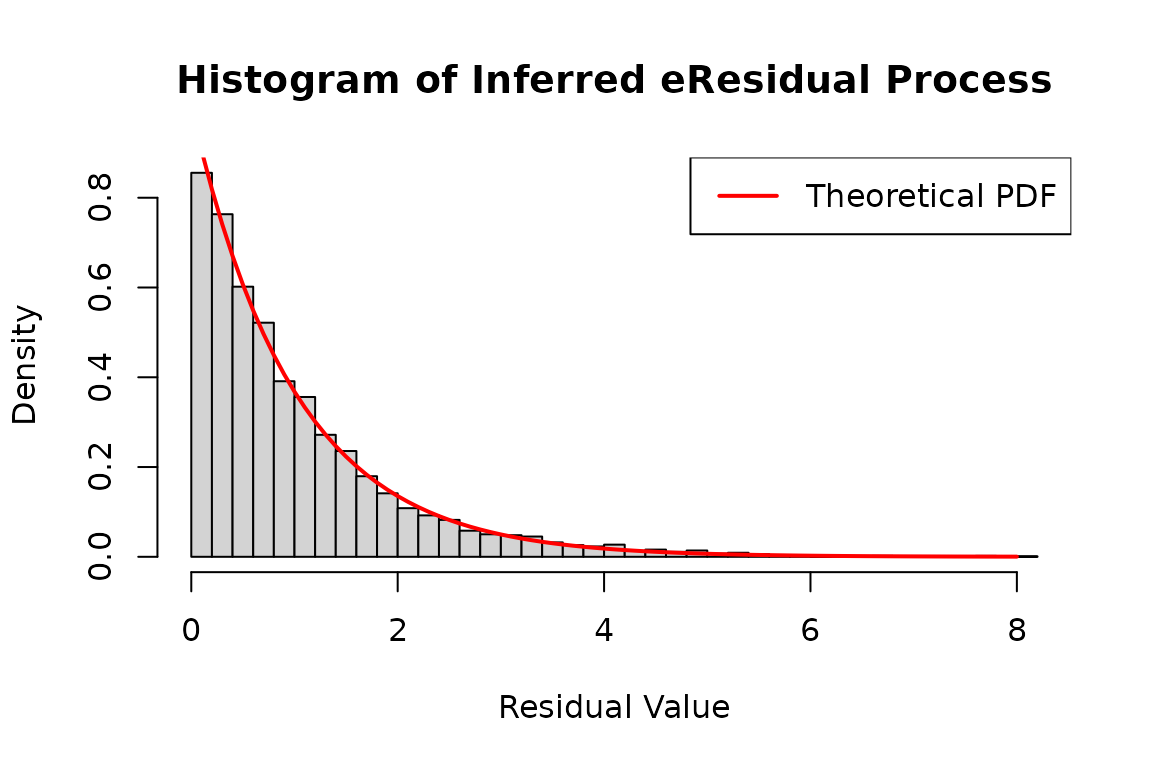

The eres_process follows the exponential

distribution.

hist(

infer_res_dh2$eres_process1,

breaks = 50,

probability = TRUE,

main = "Histogram of Inferred eResidual Process",

xlab = "Residual Value",

ylab = "Density"

)

# Generate a sequence of x values for plotting the theoretical distribution

x <- seq(0, 8, 0.1)

# Add a line to the histogram representing the theoretical density function

lines(

x,

dexp(x),

col = 'red',

lwd = 2

)

# Add legend for clarity

legend("topright", legend = "Theoretical PDF", col = "red", lwd = 2)

The maximum likelihood estimation.

mle_dh <- hfit(hspec2_du,

inter_arrival = duh2_real$inter_arrival,

type = duh2_real$type,

constraint=list(ineqA=rbind(diag(6)), ineqB=matrix(rep(0,6), nrow=6)))

summary(mle_dh)

#> --------------------------------------------

#> Maximum Likelihood estimation

#> BFGS maximization, 68 iterations

#> Return code 0: successful convergence

#> Log-Likelihood: -12548.98

#> 6 free parameters

#> Estimates:

#> Estimate Std. error t value Pr(> t)

#> mu1 0.289588 0.009073 31.92 <2e-16 ***

#> alpha1.1 0.495306 0.022192 22.32 <2e-16 ***

#> alpha1.2 0.813851 0.024297 33.50 <2e-16 ***

#> beta1.1 1.505598 0.046827 32.15 <2e-16 ***

#> a 0.692895 NaN NaN NaN

#> ell 1.584268 NaN NaN NaN

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Warning: constrained likelihood estimation. Inference is probably wrong

#> Constrained optimization based on constrOptim

#> 1 outer iterations, barrier value -0.00051762

#> --------------------------------------------Uniform residual distribution example is also provided.

#set.seed(117)

mu2_d <- matrix(c(0.5), nrow = 2)

alpha2_d <- matrix(c(0.3, 0.3, 0.3, 0.3), nrow = 2, byrow = TRUE)

beta2_d <- matrix(c(1.2, 1.2, 1.2, 1.2), nrow = 2, byrow = TRUE)

hspec2_du <- new("hspec", mu=mu2_d, alpha=alpha2_d, beta=beta2_d,

rresidual = function(size) runif(n=size, 0, 2),

dresidual = function(x, param = c()) dunif(x, 0, 2),

presidual = function(q, param = c()) punif(q, 0, 2),

qresidual = function(p, param = c()) qunif(p, 0, 2))

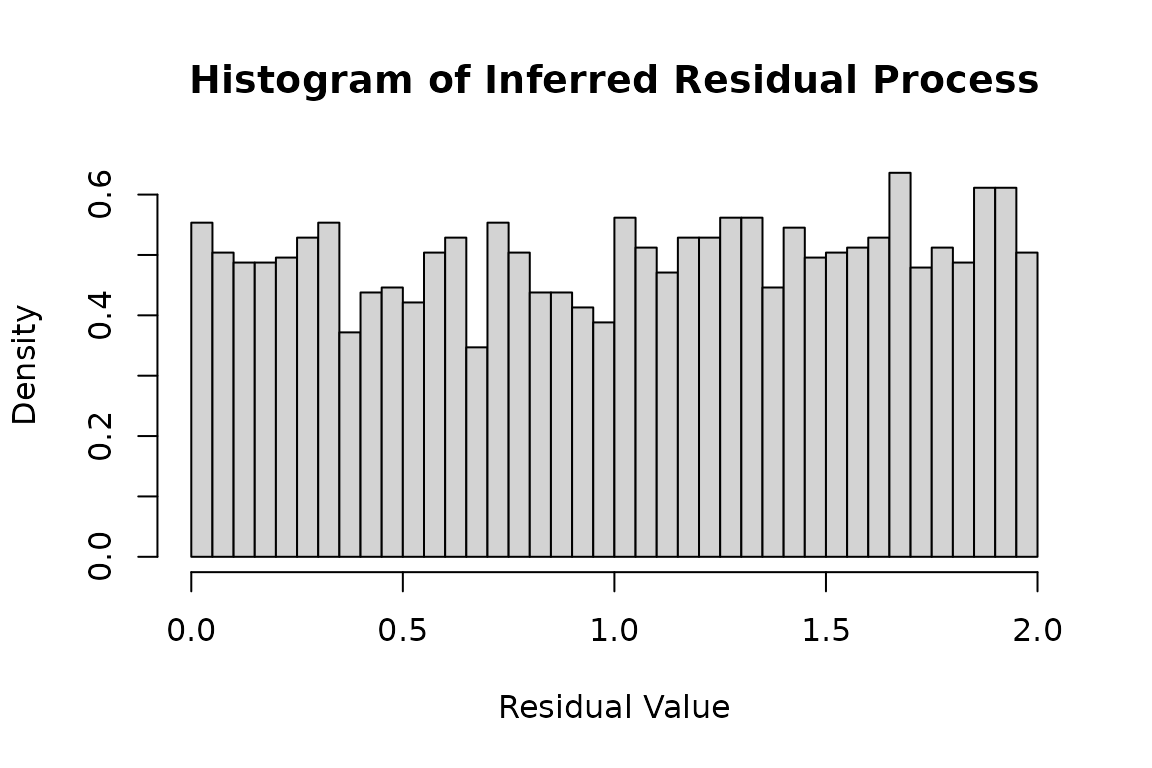

duh2_real <- hsim(hspec2_du, size = 5000)Histogram of the residual process:

infer_res_duh2 <- logLik(hspec2_du,

inter_arrival = duh2_real$inter_arrival,

type = duh2_real$type, infer = TRUE)

hist(

infer_res_duh2$res_process1,

breaks = 50,

probability = TRUE,

main = "Histogram of Inferred Residual Process",

xlab = "Residual Value",

ylab = "Density"

)